Fintechs, treated as modern financial entities, seem to be a relatively new invention in the banking world, although the foundations for this area of business were established in … the 19th century. Before you, the history of fintech: from the creation of the first transatlantic link to innovative financial startups, without which today’s financial landscape would not be complete.

XIX century – the beginning

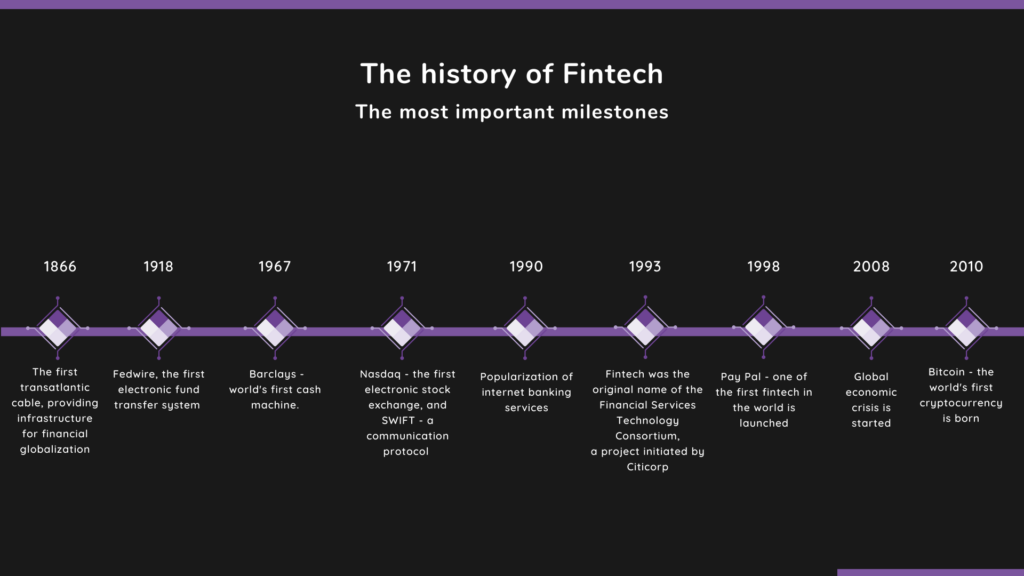

We know that dating the beginnings of the fintech industry to the nineteenth century may seem “a bit” strange daring, but indeed the year 1866 laid the foundations for the development of this branch of the economy. It was this year that the first transatlantic link was successfully laid, providing the basic infrastructure for the period of intense financial globalization that will take place soon – right at the beginning of the 20th century.

The first half of the 20th century

1918 is not only the end of military operations under the First World War, but also the time of intensive development of technologies, especially telecommunications. And so, at the beginning of the interwar period, the first ever electronic money transfer system called Fedwire was created. Its operation reflects the spirit of the time – Fedwire was based on the strength of the telegraph signal and Morse code.

In 1920, the first flashes of the philosophy on which today’s fintechs are based appear – John Maynard Keynes published his book “Economic consequences of power”, the main thesis of which concerns the development of finance, based on a combination of achievements of contemporary technology with the requirements of the financial market.

According to experts on the subject, the 19th century and the first half of the 20th century are called the “Fintech 1.0” period.

The second half and the end of the 20th century

The switch from analog to digital enabled the creation of the first Barclays ATM in history in 1967. This is the moment that symbolically marks the beginning of modern financial technologies. The digitization of the financial industry is developing at an impressive pace at that time. In the early 1970s, Nasdaq, the first electronic stock exchange, and SWIFT, a communication protocol used by financial institutions to make large amounts of cross-border payments, are created in the United States. The digitization of finance has increased due to the advancement of digital communication and transaction technology. Nasdaq and SWIFT mark the beginning of the financial markets and the communication protocols used today.

The 1990s, due to the intensive development of computers and the Internet, brought us online banking – from that moment both companies and individual clients can manage their finances from the computer screen. Internal processes and communication with clients are partially fully digitized and there is a clear shift in the way people interact with financial institutions.

Soon, the term “Fintech” appears for the first time in a wider circulation. In 1993, Citicorp established the Financial Services Technology Consortium, abbreviated as the Fintech project. This initiative is aimed at the cooperation of small, technologically advanced IT companies with banking institutions that want to develop the area of financial innovation.

A milestone in the development of electronic payments is the establishment of PayPal in 1998 – one of the first financial organizations whose mission and scope of services is very similar to the shape of today’s modern fintechs.

The achievements of financial technology at the end of the 20th century close the era of Fintech 2.0.

21st century

The long-awaited 21st century begins one of the biggest financial crises in the world – 2008 marked the collapse of the global economic system, which resulted in a sharp decline in the level of confidence in banks. The crisis paradoxically created space for the development of modern, non-bank financial services. A year later, in 2009, Bitcoin was created – the world’s first cryptocurrency, which paved the way for other cryptocurrency and distributed ledger enthusiasts.

The area of 2010 is the contractual date of entry into the Fintech 3.0 era, in which we are today. The growing popularity of smartphones and mobile and mobile access to the web and financial services make the first startups from the financial industry appear on the market, driving the wave of new products and services. Even established banks are beginning to innovate in the spirit of start-ups, and it was this departure from the established banking position of the Fintech 2.0 era that defined Fintech 3.0. There are more and more financial entities on the market, such as neo-banks, challengers or digital banks, which combine the advantages of stable banking with a modern approach to creating financial technologies.

Today

Today, the rapid development of fintechs and modern financial institutions is no surprise to anyone. Innovative products and services offered to customers are actually the expected standard, and traditional banks are increasingly looking for a way to become part of this change. Although experts are outdoing each other in forecasting the upcoming financial and technological revolution, it is worth noting that it is already happening – for a long time now, fintechs have been redefining the financial market, changing the status quo and revolutionizing the assumptions of classic banking. It is a long and endless process – because what is innovative today will soon be history.